Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

Gold’s nearly 40% rally over the past year still has momentum, according to George Milling-Stanley of State Street Global Advisors. The group’s Chief Gold Strategist emphasizes three primary sources of the yellow metal’s projected growth: central bank buying, emerging market demand, and renewed interest from Western investors. These mid-to-long-term drivers have the potential to push gold prices to $3,100, according to State Street analysts.

Gold’s nearly 40% rally over the past year still has momentum, according to George Milling-Stanley of State Street Global Advisors. The group’s Chief Gold Strategist emphasizes three primary sources of the yellow metal’s projected growth: central bank buying, emerging market demand, and renewed interest from Western investors. These mid-to-long-term drivers have the potential to push gold prices to $3,100, according to State Street analysts.

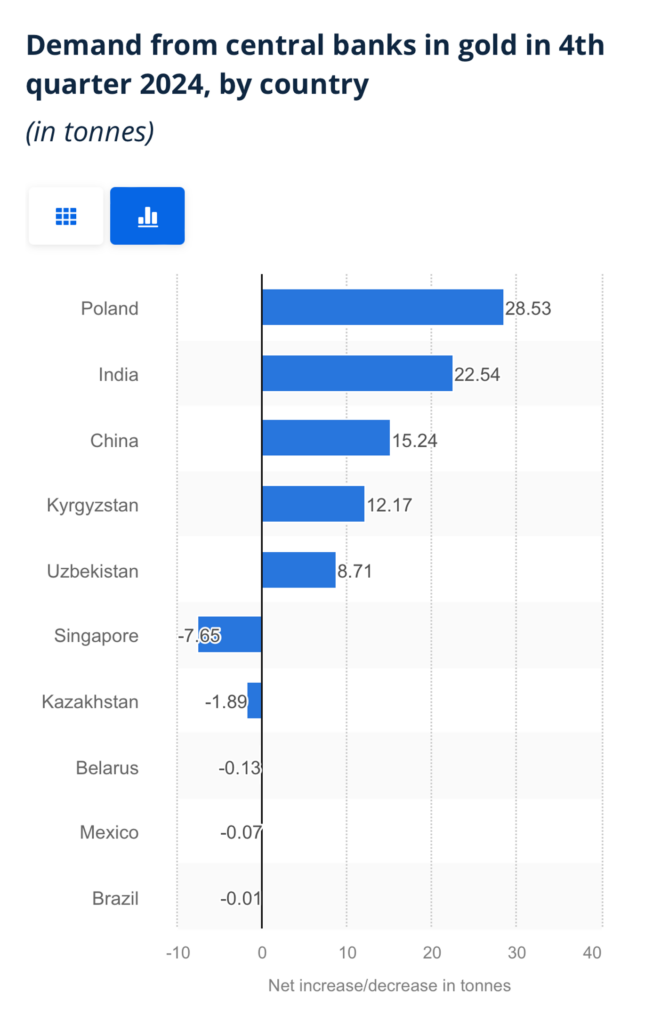

1. Central Banks Adding to Gold Reserves

In an interview with Fox Business, Milling-Stanley highlighted ongoing central bank purchases as the strongest supporter of elevated gold prices. “This has been a feature of the last 15 years of the gold market,” he explains.

Over this period, central bank consumption “has ranged anywhere from 10% to 25% of total end user demand in any given year,” showing this source’s outsized impact on prices.

National appetite has been particularly acute lately with annual purchases reaching over 1,000 tons for the past three years in a row. In 2024, overall national purchases reached 1,045 tons. Central bank demand doubled between 2021 and 2022, marking a dramatic and, thus far, sustained increase in purchases.

This sustained and elevated government gold binge is expected to continue with State Street saying, “We look like we’re set for a good year [in 2025].” This production is echoed by UBS which expects demand to reach 900 tons.

2. Emerging Markets Embracing Gold Over Dollars

Emerging markets are the runner-up in State Street’s list of the most impactful factors pushing gold’s expected rise. These countries have made up an increasingly large chunk of central bank demand, primarily spurred by dollar weaponization. As Milling-Stanley points out, emerging market gold consumption sparked following Western sanctions against Russia in the wake of its invasion of Ukraine.

As a leader and key trading partner for many emerging markets, the Kremlin’s embrace of gold as a mechanism for working around dollar-based barriers helped fuel the burgeoning de-dollarization movement.

Emerging markets are “overweight dollars, underweight gold in their official reserves,” describes the Chief Gold Strategist.

Source: Statista

In emerging nations, central bank purchases have only been rivaled by jewelry demand. For example, the Chinese jewelry market—now the largest in the world—gobbled up 500 tons of gold in 2025, over ten times the amount purchased by the country’s central bank. This surge in jewelry purchases is bullish for gold prices as the jewelry market accounts for more than 50% of total gold demand.

3. Western Investors Returning to Gold Markets

Western investors have been relatively underrepresented in the gold market compared to their Eastern counterparts. However, retail investors in the US and Europe are showing signs of revival as investments pick up. For instance, in Q1 2024, year-on-year coin and bar purchases grew by 68% in China and fell by 44% in Western markets.

By Q3, North America was dominating inflows with several consecutive months of positive purchases. This reinvigorated interest in physical gold is largely driven by alarming indicators in both US and European markets as both economies reel from mounting debt burdens, unchecked spending, and rising inflation. “The attitude of uncertainty has been fed by the political turbulence we’ve been seeing around the globe,” as Milling-Stanley explains.