Eric Sepanek

SBC Founder

Eric Sepanek is the founder of Scottsdale Bullion & Coin, established in 2011. With extensive experience in the precious metals industry, he is dedicated to educating Americans on the wealth preservation power of gold and silver.

Precious metals as a collective asset class cleared new highs in 2024, reports the World Bank. The group’s precious metals index rose steadily throughout the year before peaking in October. Gold led the charge with a year-long rally, reflecting robust demand from central banks and rising economic uncertainty. Although prices have settled below record levels, analysts anticipate further growth in 2025 across the precious metals space.

What is the World Bank Precious Metals Index?

The World Bank’s Precious Metals Price Index is a collection of physical metals, mostly gold, silver, platinum, and palladium, designed to track the overall performance of the metals market. The spread of these four assets is weighted based on their influence on the global market. For example, gold accounts for the largest share because the yellow metal is the most widely traded.

Across-the-Board Gains

In 2024, this Precious Metals Index rose by 20%, representing considerable sector-wide growth. The weighted index even claimed an all-time high in October on the back of record Q3 demand.

Source: World Bank

As the World Bank reports, “The recent price increase was largely driven by gold,” due to its sustained 2024 rally and outsized role in the index. From a broader view, precious metals growth was propelled by an array of macroeconomic, financial, and geopolitical variables.

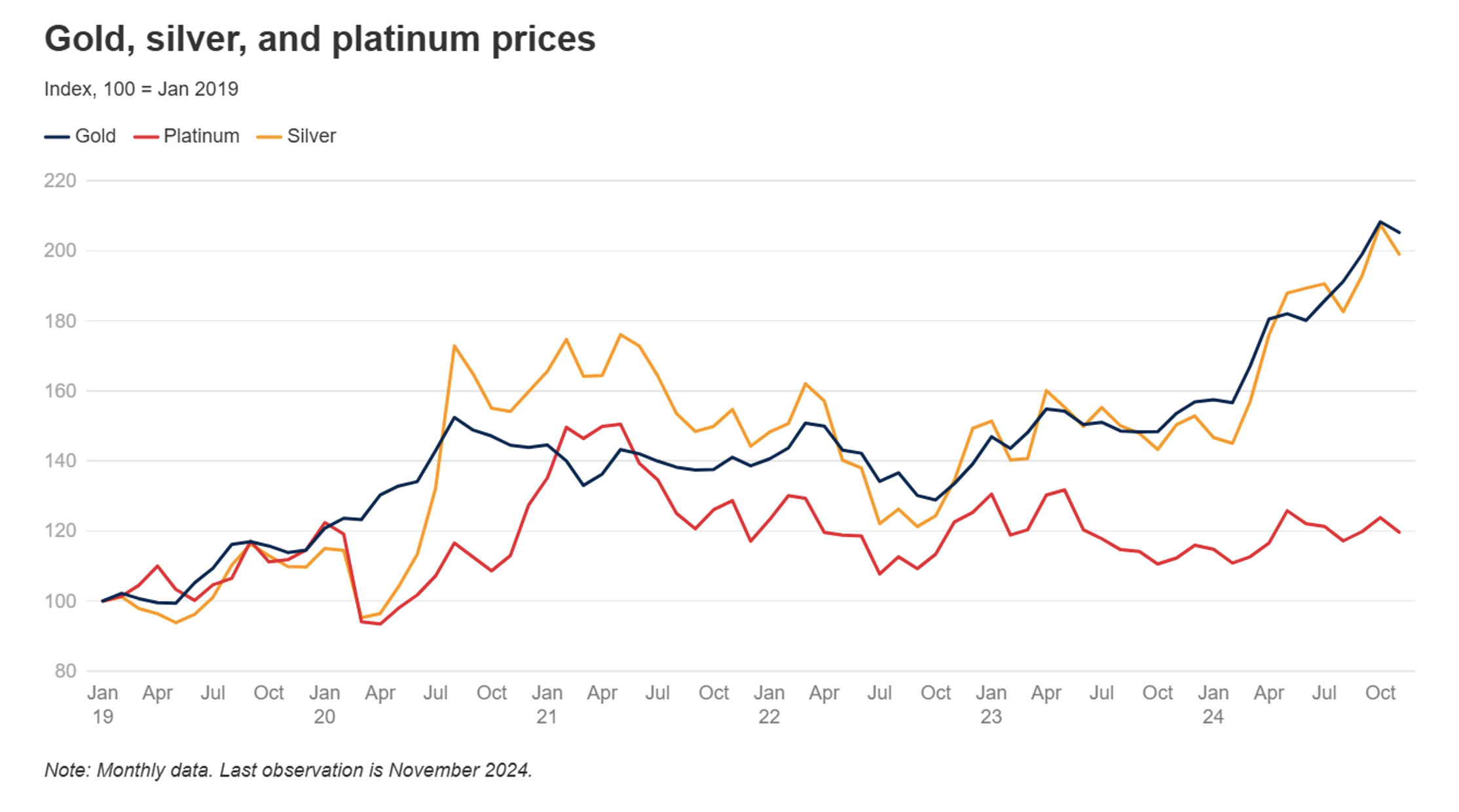

Gold

The precious metals market’s shining star posted a formidable 27% gain in 2024, topping at $2,786.44. According to the World Bank, a handful of circumstances contributed to this jump:

Geopolitical Tensions – A steady escalation in global conflicts, international rifts, and trade tensions has triggered a general shift away from vulnerable dollar-link assets.

“Gold has benefited from geopolitical uncertainties throughout [2024]”, explains World Bank analysts, due to its status as a safe-haven asset.

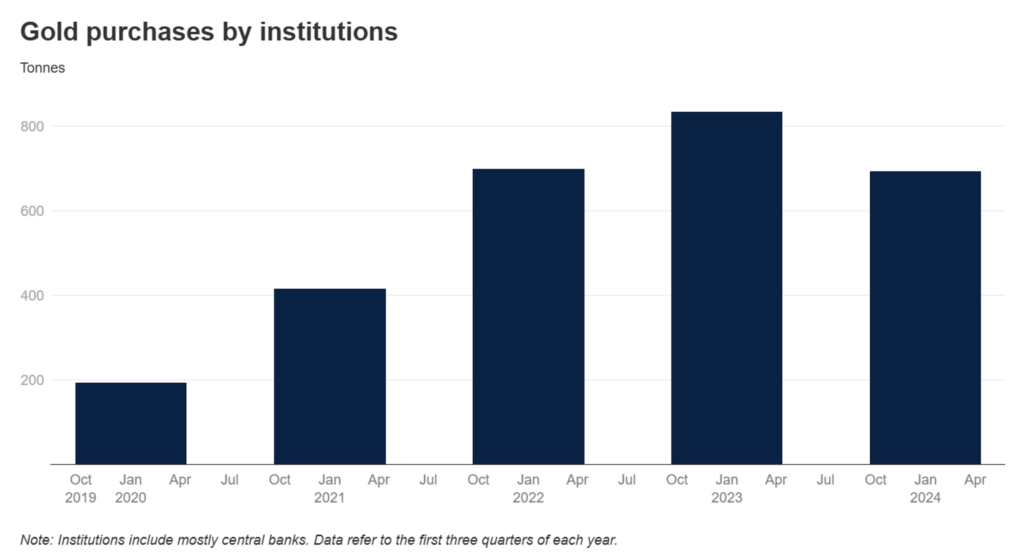

Central Bank Consumption – Resilient central bank demand throughout 2024, spearheaded by emerging markets, dramatically elevated gold prices.

This move reflects a broader five-year-long trend of institutional investors, primarily governments, becoming net-purchasers of gold. Additional support came from retail purchases of gold ETFs, offering further tailwinds for price growth.

Monetary Easing – The US economy’s changeover into monetary easing boosted gold prices as the Federal Reserve’s rate cuts increased the yellow metal’s appeal. With steady slashes planned throughout 2025, the fiscal policy climate is looking positive for gold.

The World Bank joins a bevy of bullish 2025 gold predictions, anticipating prices to rise “80% above their 2015-19 average throughout 2025-26.”

Silver

From the start of the year to its peak, silver prices outpaced gold with an impressive 46% rise. However, a sharper correction in the latter half of the year tempered silver’s rally, leaving it with a still respectable 21% surge. World Bank analysts highlight the key drivers behind silver’s rise, noting a mix of factors shared with gold as well as those unique to silver:

Monetary Easing – The Fed’s pivot to steady rate cuts reinforced silver prices as the opportunity cost of owning physical assets and the appeal of traditional investments waned.

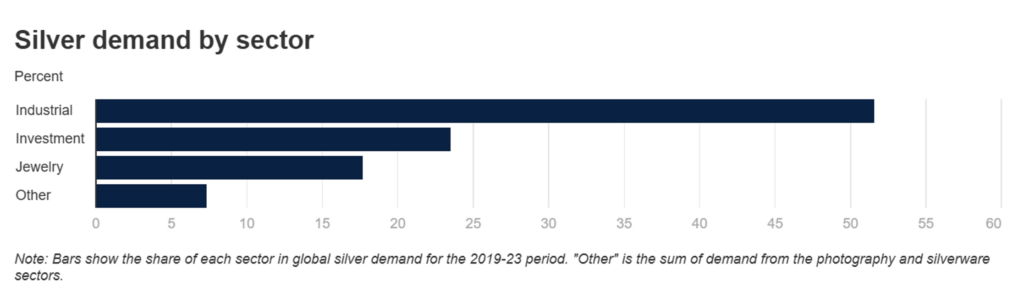

Industrial Demand – Silver’s dual role as an investment and industrial metal bolstered demand, especially with booming consumption in the renewable energy space.

Tight Supply – A confluence of heightened demand and strained supplies resulted in a stark silver supply deficit. This market tension further buoyed silver’s rise.

Looking forward, silver is slated to grow by 7% in 2025 and by an extra 3% in 2026, according to World Bank analysts. This projection falls in line with upbeat 2025 silver price forecasts among experts.

Platinum

Platinum prices struggled in 2024, exhibiting characteristic volatility before falling 9%. A challenging combination of demand dynamics and structural market shifts weighed heavily on potential increases:

Reduced Substitution – As the price gap between platinum and palladium narrowed, industrial preference for platinum waned, drying up a key source of demand.

Weakened Demand – A slump in automotive demand, which accounts for two-fifths of total consumption, exerted significant pressure on prices as governments pushed electrical vehicles (EVs).

Despite these headwinds, platinum is projected to chart a 5% jump in 2025 and 2025. While industrial demand is on pace to drop, a collective rise in investment, automotive, and jewelry demand could offset those losses.